2008 Financial Crisis: Quantitative Analysis & Model Failures

Explore the mathematical causes of the 2008 financial crisis, including Gaussian Copula failures, CDOs, leverage risks, and systemic economic impacts.

The 2008 Global Financial Crisis

A Quantitative Analysis of Causes and Impacts

Perspective: Systemic Risk & Model Failure

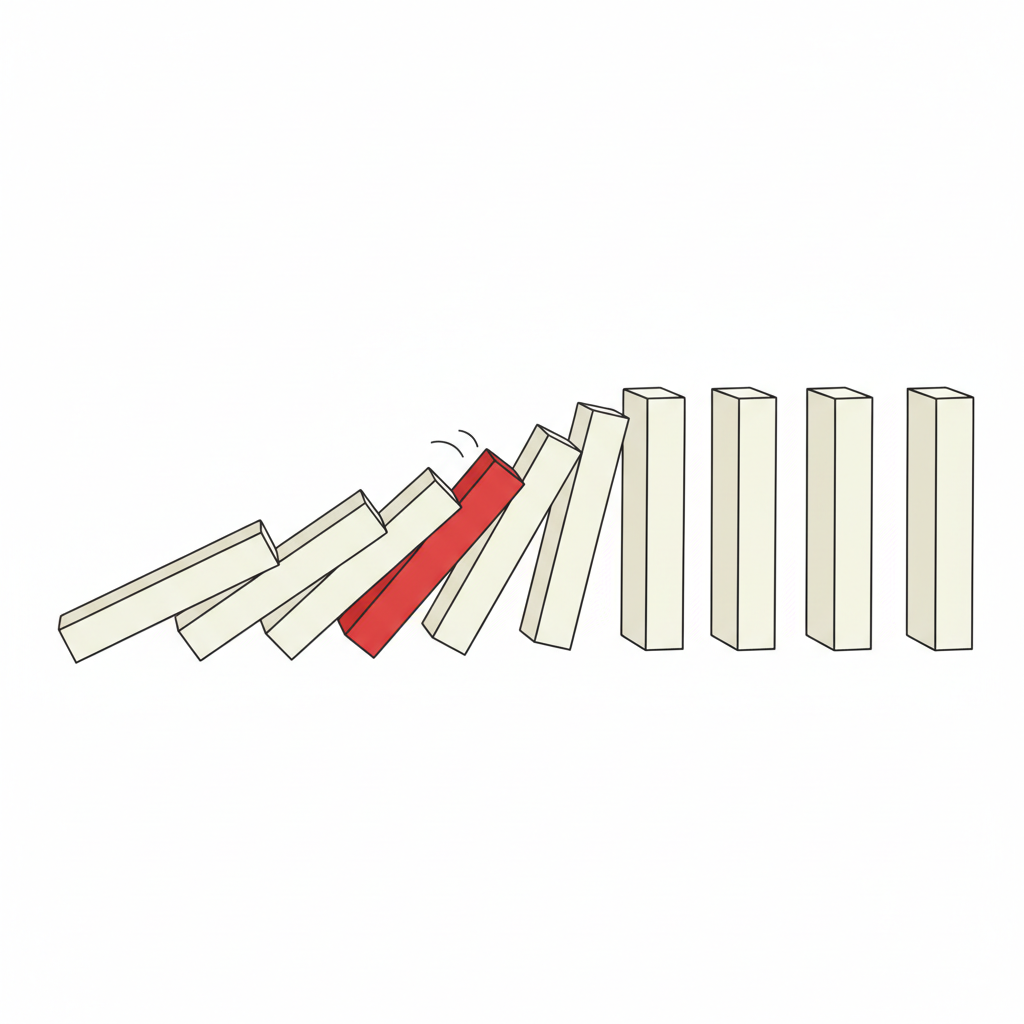

Crisis Timeline & Propagation

2000–2006: Housing boom & credit expansion

2006–2007: Rising mortgage defaults begin

2008: Lehman Brothers collapse → Global Panic

2009: Deep global recession

Housing Bubble: The Divergence

The Case-Shiller Home Price Index showed prices decoupling from historical norms (income and rents) starting in 2000.

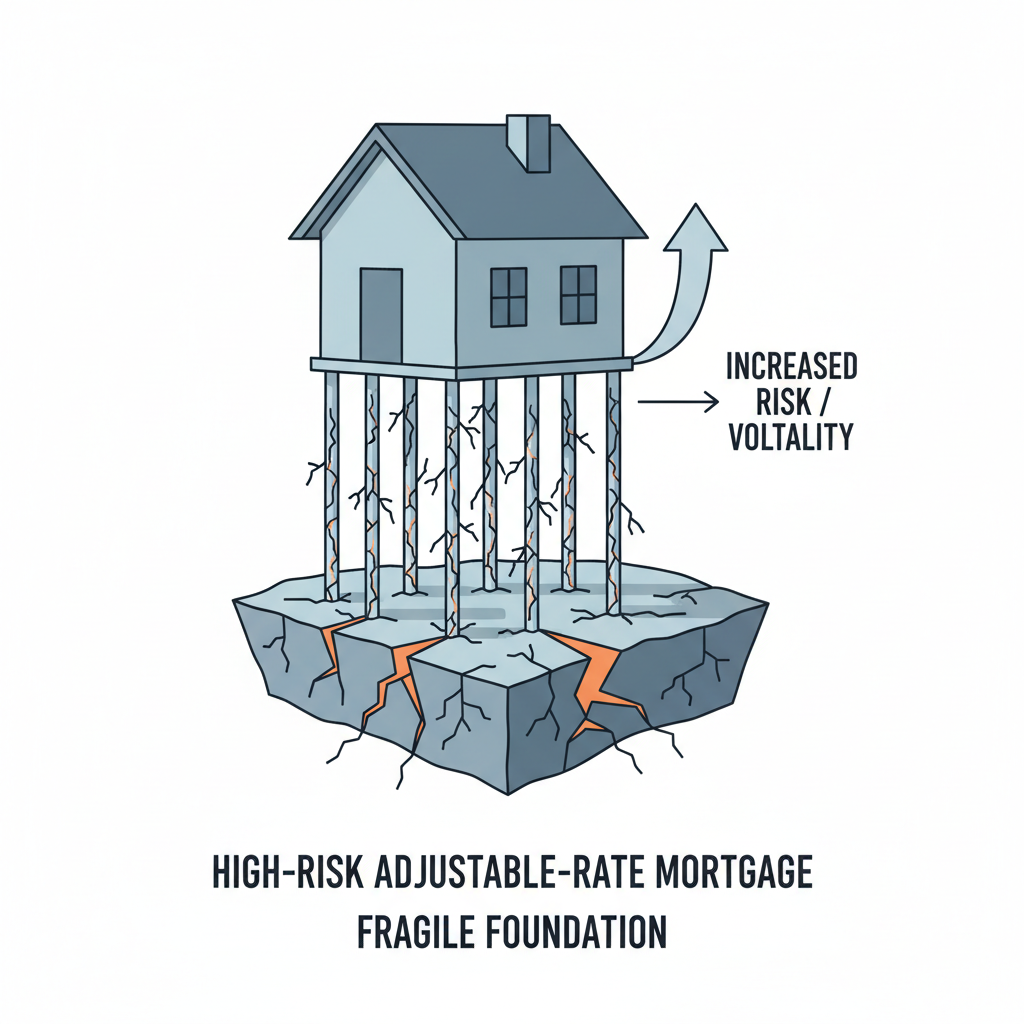

Subprime Mortgages & Default Probability

High-risk borrowers with no income verification (NINJA loans).

High Loan-to-Value (LTV) ratios left no equity cushion.

Adjustable-Rate Mortgages (ARMs) triggered defaults when rates reset.

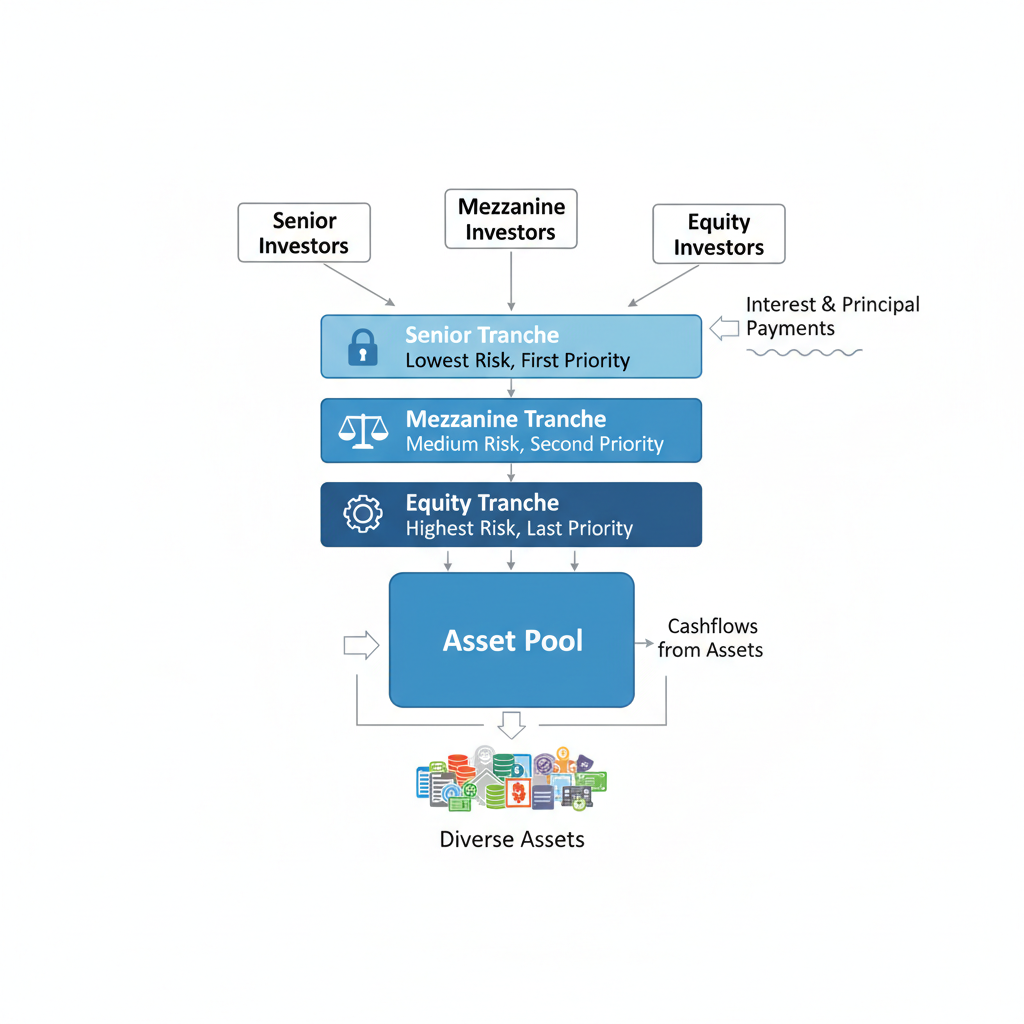

The Illusion of Diversification: CDOs

Mortgage-Backed Securities (MBS) pooled thousands of loans.

CDOs sliced these pools into 'tranches' based on risk preference.

Assumption: Geographical diversification reduces joint default risk.

The Culprit: Gaussian Copula

P(joint default) = Φ_ρ ( Φ⁻¹(p₁), ... , Φ⁻¹(pₙ) )

Used to price CDOs by estimating the probability of simultaneous defaults.

ρ (Rho): The Correlation Parameter

If ρ is low, tranches seem safe. If ρ spikes to 1, the model collapses.

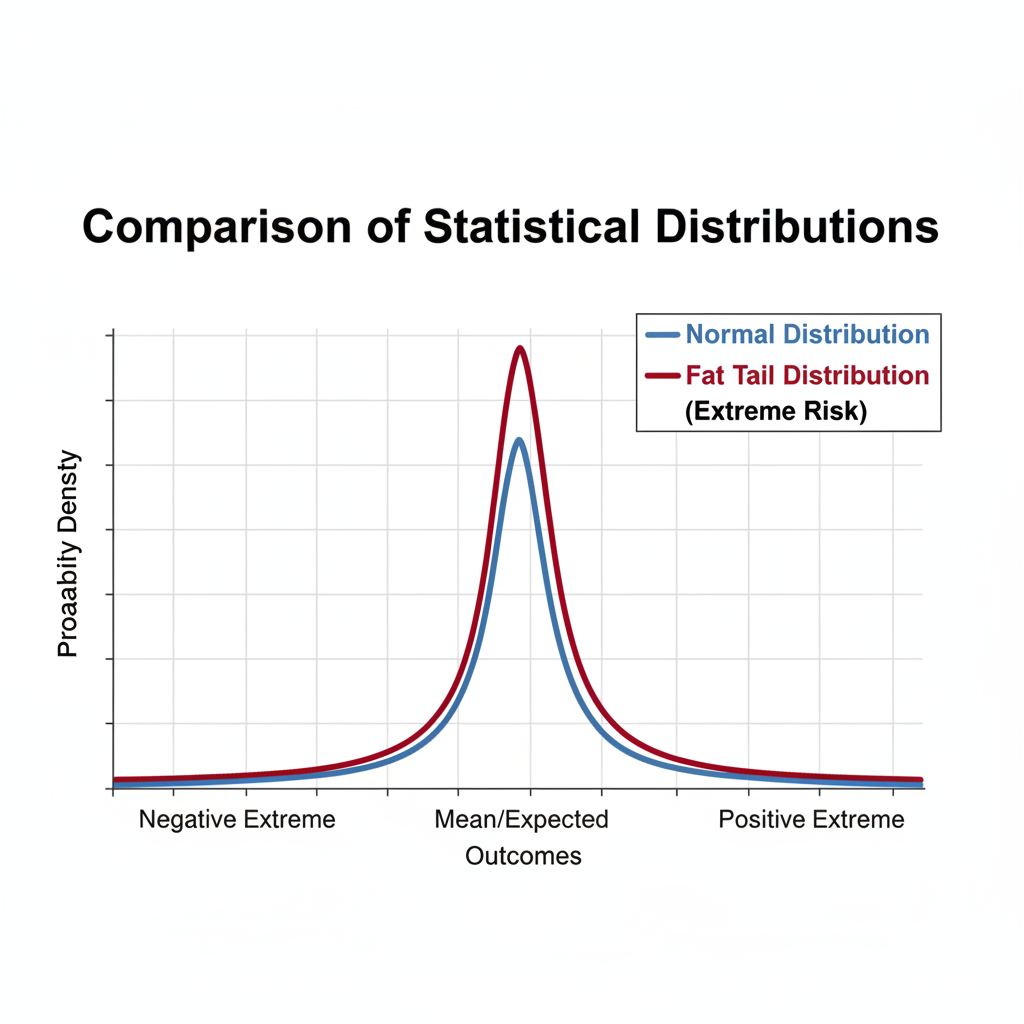

Why the Model Failed

Historical Bias: Data only covered the housing boom (short memory).

Thin Tails: Gaussian distributions underestimate extreme events.

Dynamic Correlation: In a crisis, correlations trend toward 1.0.

Leverage: The Magnifier

Leverage = Total Assets / Equity

With 30x leverage, a mere 3.3% drop in asset value wipes out 100% of equity.

Economic Impact: The Real Economy

ΔGDP ≈ α + β(Credit Spreads) + ε

As credit markets froze, the real economy crashed. US Unemployment doubled in two years.

Lessons for Quantitative Finance

Models are tools, not truth.

Correlation ≠ Causation (and correlation is not constant).

Stress Testing: Always test for 'impossible' scenarios.

"Quantitative methods should support judgment, not replace it."

- financial-crisis

- quantitative-finance

- systemic-risk

- economics

- housing-bubble

- risk-management

- statistics