Guide to Credit Card Disputes & Chargeback Best Practices

Learn how credit card disputes work, valid chargeback reasons, Visa timelines, and consumer protection laws like Singapore's Lemon Law.

Credit Card Disputes in the Eyes of the Cardholder

Understanding Dispute Reasons, Chargebacks & Consumer Responsibilities

Prepared by: Dispute Resolution Team

Pre-Training Quiz — Question 1

What is the strongest ground for a chargeback approval?

A) Buyer's Remorse<br>B) Unauthorized/Fraudulent Transactions<br>C) Finding a cheaper price elsewhere<br>D) Forgetting to cancel a subscription 1 day late

Pre-Training Quiz — Question 2

For 'Goods Not Received', what is the first step a cardholder must take?

A) Call the police<br>B) Post on social media<br>C) Attempt to resolve with the merchant<br>D) Immediately file a lawsuit

Pre-Training Quiz — Question 3

Which of these is NOT a valid reason for a dispute?

A) Double billing<br>B) Buyer's Remorse (Changed mind)<br>C) Counterfeit goods<br>D) Merchandise arrived broken

Pre-Training Quiz — Question 4

Under Singapore Lemon Law, what is the coverage period for defective goods?

A) 30 Days<br>B) 3 Months<br>C) 6 Months<br>D) 1 Year

Introduction

Disputes are a mechanism to protect consumers from fraud and unfair commercial practices.

Chargebacks generally allow the recovery of funds when properly justified.

Card schemes (Visa/Mastercard) define strict rules and timelines for this process.

Cardholders have specific responsibilities to ensure the system works fairly.

What Is a Credit Card Dispute?

A formal request to investigate a specific transaction.

Triggered by incorrect, unauthorized, or unfair charges appearing on a statement.

If valid, a dispute may escalate into a 'chargeback'—the reversal of funds.

Why Disputes Matter

Protects consumers from fraud

Ensures merchant accountability

Maintains trust in digital payments

Encourages responsible buying and selling behavior

Behind the Scenes: The Dispute Flow

Understanding the ecosystem helps manage timelines.

Initiation

The process begins when the cardholder identifies an incorrect transaction. They contact the Issuer Bank to raise a dispute, submitting initial details and any available evidence.

Network Processing

The Issuer validates the claim and routes it through the Card Network (e.g., Visa, Mastercard). The network acts as an intermediary, forwarding the dispute to the Merchant's Acquirer Bank.

Merchant & Resolution

The Acquirer notifies the Merchant, who can either accept the chargeback or fight it by providing compelling evidence. The final outcome travels back through the chain to the cardholder.

Common Dispute Categories

Fraud / Unauthorized transactions

Billing errors (Double billing, Wrong Currency)

Goods/Services not received

Goods/Services not as described

Refund not processed

Subscription cancellation not honored

Other - Scam

Fraud & Unauthorized Transactions

This occurs when the cardholder specifically did not approve the charge.

Common scenarios: Stolen card details, Phishing attacks, Account Takeover (ATO).

Note: This is the strongest ground for chargeback approval.

Billing Errors

Wrong Amount: Charged differently than the receipt.

Incorrect Currency: Dynamic Currency Conversion issues.

Double Billing: One transaction processed twice.

Technical processing errors.

Goods or Services Not Received

The merchant fails to deliver the promised item or service.

• Includes undelivered online orders.<br>• Covers cancelled services (flights, events).

CRITICAL: The cardholder must attempt to resolve the issue with the merchant first before filing a dispute.

Goods or Services Not as Described

The product received differs significantly from the advertisement or description.

Counterfeit goods, wrong color/size, poor quality material, broken on arrival.

Requires Proof: Photos of the item, original description screenshots, and email correspondence.

Chargeback Opportunities

When are chargebacks most likely to succeed?

Merchant violates card-scheme rules

Cardholder provides strong supporting evidence

Merchant fails to respond to the inquiry

Chargebacks must be used responsibly—they are not for simple returns or regret.

Visa Chargeback Timeline

Day 0–120: Cardholder files dispute

Day 0–30: Issuer reviews and submits chargeback

Day 30–45: Merchant responds

Day 45–90: Issuer reviews evidence

Day 90–120: Case resolved or escalated

Remarks: Chargeback window timeframe is generally 120 days from date of disputed transaction for most dispute reasons, except for some which are 75 days or 540 days for certain situations.

Visa Chargeback Prerequisites

1. Attempt merchant resolution

2. Provide supporting documentation

3. Confirm this is not 'buyer's remorse'

4. File within the allowed timeframe (usually 120 days)

Case Study 1: Unauthorized Transaction

Scenario: $1,200 charge at a tech store (Apple.com) the cardholder didn't make.

Action: Cardholder blocked card and reported fraud immediately.

Outcome: Chargeback APPROVED.

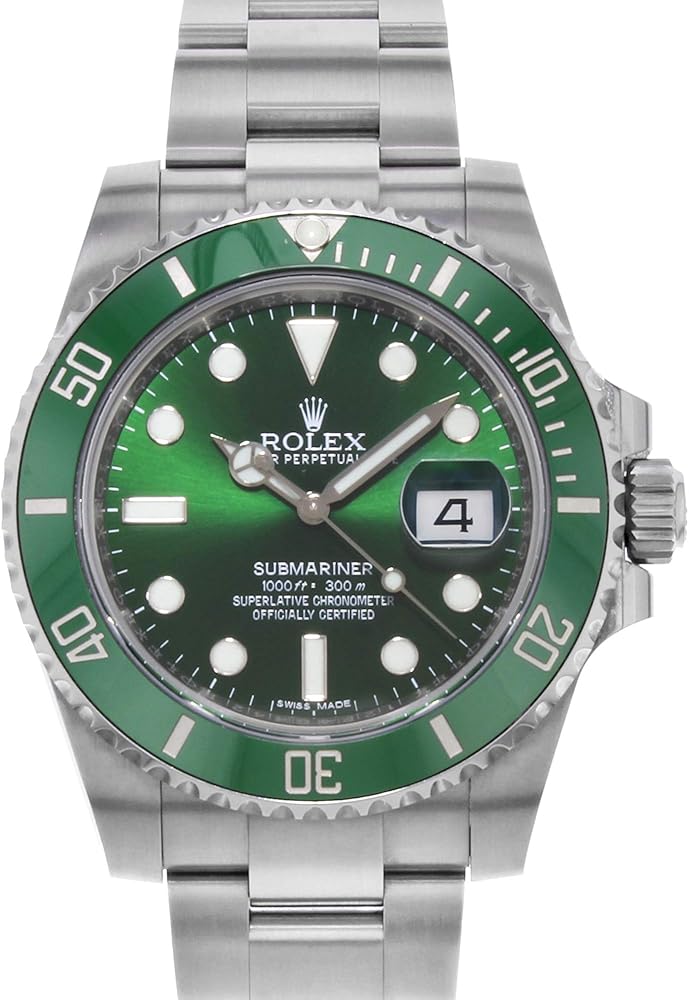

Case Study 2: Goods not received. Refund not received

Scenario: Charged at CHN online store for a premium replica Rolex watch (cloned) for CNY 1751.

Action: Watch was not delivered due to custom check.

Outcome: Merchant rejected refund and requested customer to contact them.

Case Study 3 : Goods received were defective

Scenario : A regular customer bought a Birkenstock kids sandals from a reputable online store.

Action: She raised a dispute over the receipt of damaged item but merchant countered her claim saying there was quality check before delivery. There was a stand off.

Outcome : Dispute unsuccessful.

Buyer’s Beware

• Consumers must exercise caution.<br><br>• Research merchants before buying.<br><br>• Read reviews online.<br><br>• Understand return policies before checkout.

Buyer’s Remorse

Emotional regret is NOT a valid dispute reason.

Chargebacks cannot be used simply because you changed your mind.

This highlights the importance of consumer responsibility.

Additional Consumer-Protection (Singapore)

• CASE: Mediation for unfair practices.<br><br>• Small Claims Tribunal: Claims up to S$20k/S$30k.<br><br>• Lemon Law: Defective goods within 6 months.<br><br>• CPFTA: Fair dealing principles.

Consumer Dispute Remedies Comparison

Source: CASE, SCT, and Consumer Protection (Fair Trading) Act

Summary

Questions?

Contact: Your friendly Dispute Resolution Specialists

Disputes protect consumers and ensure fairness in the ecosystem.

Chargebacks are powerful tools when used correctly and ethically.

Cardholders must act responsibly (documentation & timelines).

Additional protections exist under Singapore law (Lemon Law, CASE).

Thank You

Disputes protect consumers and ensure fairness in the ecosystem.

Chargebacks are powerful tools when used correctly and ethically.

Cardholders must act responsibly (documentation & timelines).

Additional protections exist under Singapore law (Lemon Law, CASE).

Questions?

Contact: Your friendly Dispute Resolution and Chargeback Specialists

- credit-card-disputes

- chargeback-process

- consumer-protection

- fraud-prevention

- visa-rules

- lemon-law

- personal-finance